Tesla: 3 Reasons Why It May Break Wright's Law - Seeking Alpha

Written by

Summary

- Wright’s law has successfully predicted auto production costs in the past 100 years.

- Now can it predict Tesla’s?

- The bad news is that Tesla has not been reducing its cost as fast as the law predicts so far.

- But for a non-linear growth stock like Tesla, there are several opportunities for it to catch up and may even break the law.

- Looking for more investing ideas like this one? Get them exclusively at Envision Early Retirement. Learn More »

Thesis and Background

I first read about Theodore Paul Wright as an aeronautical engineer and educator (when I was studying engineering in graduate school). Only years later did I learn about his most important contribution, which is not in aeronautics (though it is rooted in aerospace engineering). While studying airplane manufacturing, Wright determined that for every doubling of cumulative airplane production the labor requirement was reduced by 10-15%. Now known as “Wright’s Law”. The law has been so effective in predicting the cost of a wide range of products beyond airplanes, including the automobile production costs in the past 100 years.

Now the question is – can it predict a “new” product like EVs produced by Tesla (NASDAQ:TSLA)? And you will see in this article that:

- Tesla has not been reducing its cost as fast as the law predicts so far. Not even fast enough to keep with the lower bound of 10% in Wright’s law.

- But for a nonlinear growth stock like Tesla, there are several opportunities for it to catch up and may even break the law. For one thing, Elon Musk himself is a large intangible asset that saves the companies billions of dollars on advertisement. And for a nonlinear stock like TSLA, there are 2nd order effects and even 3rd order effects that can cut costs faster than the law predicts once its fleet in operation reaches a critical point.

What is Wright’s Law?

As aforementioned, Wright determined that for every doubling of airplane cumulative production, the labor requirement was reduced by 10-15% on a per-unit basis. Specifically, it states that for every cumulative doubling of units produced, average unit costs will fall by a constant percentage between 10-15%. Take the lower bound of 10% as an example. If we have so far produced 1000 units of something (say microwave oven) and the average cost per unit is $100. Then Wright predicts that when cumulative production reaches 2000 units, the average unit cost will be only $90. When cumulative production reaches 4,000, then the average unit cost will only be $81, and so on. And if you plot such a relationship on a log-log plot (average unit cost vs cumulative units produced), you would see a straight line.

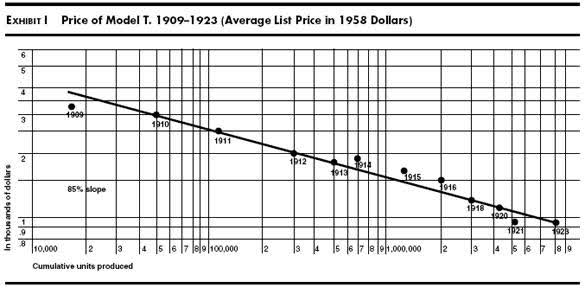

Now specific to the auto industry, the following chart shows this relation for Ford’s Model T between 1909-1923. And as you can see, the relationship is precisely a straight line as predicted by Wright’s law!

And if you measure the slope of this line in the chart, you would see that it is about 15%. The traditional auto industry has enjoyed a 15% cost reduction per cumulative production doubling – near the upper limit of Wright’s law.

Now, let’s see if the “new” auto industry is following this law or not.

Is TSLA following Wright’s law so far?

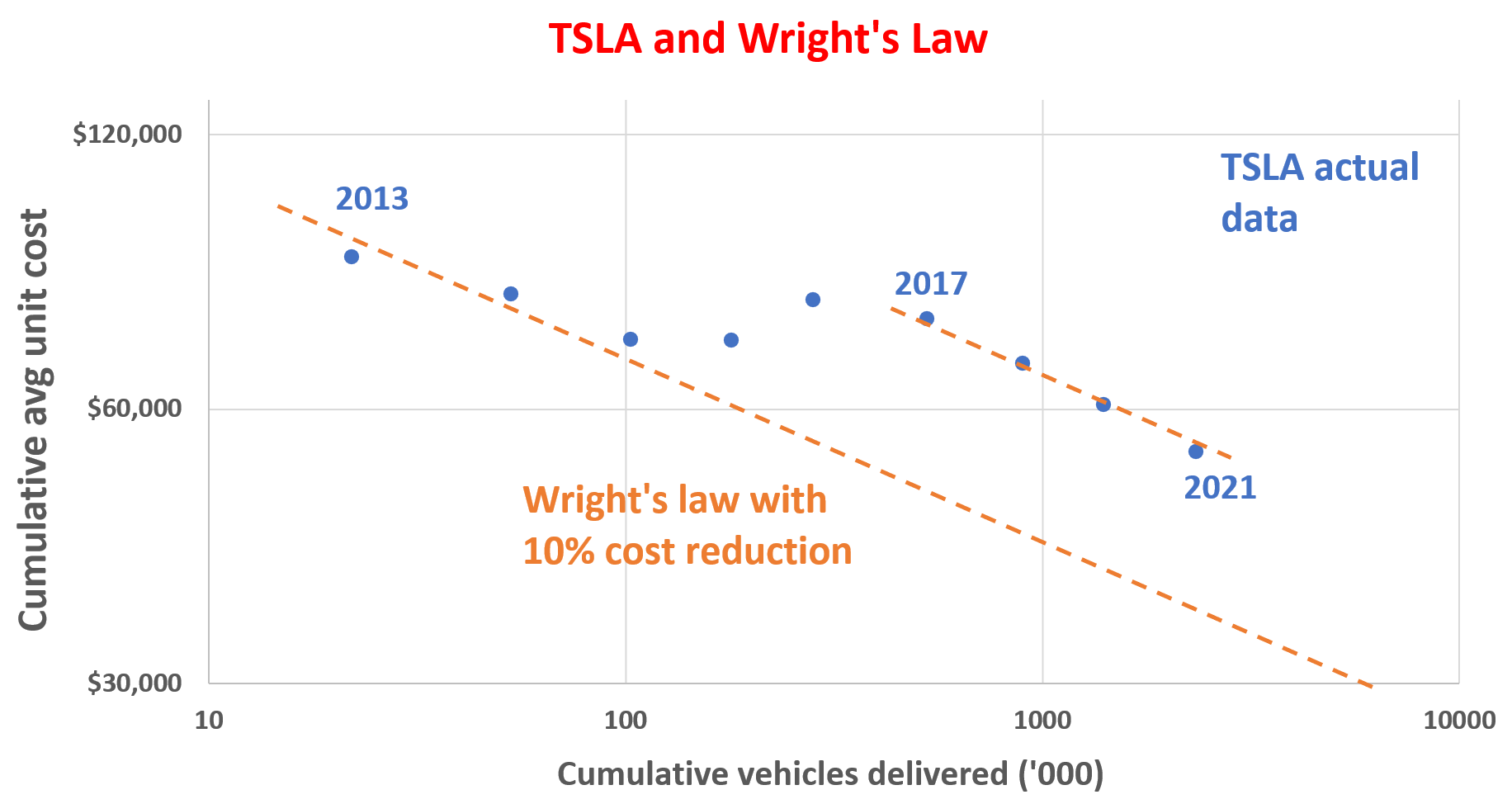

Since this law is so effective, let's try it on TSLA. The chart below shows the average cost per vehicle as a function of its cumulative vehicle deliveries since 2013 (the year TSLA first started delivering vehicles). And the orange lines show Wright’s law with a 10% cost reduction. As you can see, the cost reduction of Tesla is not following Wright’s law so far. Its average cost lies above even the lower limit 10% reduction line currently. Although note that its cost reduction HAS been following the law in some period or some particular markets. For example,

- During 2017 and 2021, the cost reduction has been following Wright’s law closely with a 10% cost reduction.

- Also, it has been following (or breaking) the law in the China market during 2019 with its model 3. As of the second quarter of 2019, Tesla Model 3 has produced a total of 275,000 vehicles, and the domestic model 3 price was about 328,000 Chinese yuan at that time. As of the end of 2020, Tesla Model 3 has accumulated production of about 600,000 units, more than doubling. And the production cost of the Model 3 is roughly 23% lower – more than the 10~15% range predicted by Wright’s law.

Will TSLA catch up to Wright’s law?

Looking forward, can TSLA’s cost reduction accelerate and catch up to Wright’s law? I am optimistic and for at least 3 key reasons.

First, Elon Musk. TSLA, for better or worse (and we will elaborate on the “worse” in the risk section), is inseparable from Elon Musk. For one thing, Elon Musk himself is a large intangible asset that saves the companies billions of dollars on advertisement. He has essentially created a different marketing paradigm for the auto industry.

The following chart shows advertisement expenditure per car sold for the major players. And you can see that Tesla really stands out with its $0.00 expenditure. Elon Musk is not a big fan of traditional advertising – because he does not need to. He himself serves as the most effective advertisement given his unmatched charisma, incredible vision, and mastery of social media. Saving hundreds of dollars on advertising per vehicle is definitely a big help toward cost reduction.

Source: VisualCapitalist.com

Second, pivot production scale. This next chart plots the average Cash From Operations per vehicle and also the average sales per vehicle since 2017. And you can see very clearly that Tesla was able to make improving profits per vehicle while the sales per vehicle (i.e., the price tag on each vehicle) have actually been DECLINING – a clear indicator of passing the pivot point of critical scale and starting to enjoy the benefits of scale production. That is why its cost reduction has been following Wright’s law since 2017 (although only at a lower limit of 10%). And for the reasons analyzed in this section, I am optimistic that the trend will push on and even accelerate to the higher limit predicted by Wright’s law.

Source: author based on Seeking Alpha data

Third, nonlinear growth opportunities. A completely new industry like EV enjoys nonlinear growth opportunities totally unexpected (otherwise, it would not be nonlinear). When iPhones first come out, who would have thought that smartphones would one day revolutionize the TAXI HAILING business iPhone just came out? For nonlinear stocks like TSLA, I expect the growth is just getting started and the unpredictable explosive growth has not shown up at all yet. Even “obvious” assumptions should be carefully examined and a good example here is its software business associated with its autonomous driving. The details discussions have been provided in my earlier discussion and here I will just summarize the gist:

Research is beginning to show that automated or semi-automated vehicles like those TSLA makes when there are enough of them in operation, can lead to increased vehicle miles traveled (“VMT”). In other words, as TSLA sells more vehicles and there are more of its vehicles in operation, we are very likely to drive more also – creating a nonlinear growth.

Such nonlinear effects create many possibilities to reduce unit cost faster, much faster, than production scale. Just to name a few examples:

- Service sales. Service sales will be proportional to VMT, not only the number of vehicles. And hence service sales will grow faster than volume.

- Insurance. Again, insurance sales will be proportional to VMT, not only the number of vehicles. And hence also will grow faster than volume.

- Other paid services such as autonomous driving functions and software. This is an area that can grow at an even higher-order due to the so-called network effects. The network becomes exponentially more profitable and valuable as it becomes bigger.

Risks

There are risks involved with TSLA investment. At a grand level, it has a heavy speculative flavor and is definitely not for all investors. To detail a few of them:

- Its production growth is uncertain. Its ongoing production expansion projects are facing delays. Giga Shanghai is producing cars, but only at a partial capacity that is substantially lower than its target capacity. Its Giga Berlin and Texas are still under construction and Giga Berlin has hit numerous delays.

- TSLA is suffering from delays with its key projects, including its autonomous driving project and its Semi project. Its Semi is still in the prototype stage and has delayed production multiple times. The company is now expecting Semi production to start in 2023.

- The competition in the EV space is also heating up. TSLA’s market share in some of the major markets is under a lot of pressure not only from established car manufacturers but also EV companies in the US and abroad. Traditional players, particularly Volkswagen and the Ford Mach E are taking market share in the EU and U.S., respectively. In China, another key EV market, NIO is currently Tesla’s biggest competition, followed by Li Auto and XPeng.

- Lastly, Elon Musk. As aforementioned, Elon Musk himself is a large intangible asset that saves the companies billions of dollars on advertisement by defining new paradigms. However, having a company so inseparably tied up to one person creates a risk in itself. As a small example, shareholders have experienced the large price volatilities – in both directions – plenty of times created by Musk’s decisions regarding his own shares. And the next person may not (very likely will not) have the personality to draw the attention Musk draws and will have to spend heavily on advertising as other players do.

Conclusion and final thoughts

Wright’s law has successfully predicted auto production costs in the past 100 years. Here we ask a new question – can it predict a “new” EV stock like TSLA? The key takeaways are:

- Tesla has not been reducing its cost as fast as the law predicts so far. Not even fast enough to keep with the lower bound of 10% in Wright’s law.

- However, its cost reduction HAS been following the law in some time period (e.g., since 2017) or in some particular markets (e.g., with its model 3 in China).

- Looking forward, I expect it catch up with the cost reduction predicted by the law and may even break the upper 15% limit. There are several opportunities for it to accelerate its cost reduction from here on – at least for three good reasons. First, Elon Musk has redefined a new marketing paradigm that saves the company billions of dollars on advertisement. Second, it has clearly passed the pivot point of critical scale since 2017 and begin to benefit from scale production. And third, its software business and autonomous driving technology can unlock nonlinear growth.

Check out our marketplace service

As you can tell, our core style is to provide actionable and unambiguous ideas from our independent research. If your share this investment style, check out Envision Early Retirement. It provides at least 2x in-depth articles per week on such ideas.

We have vetted and perfected our methods with our own money and efforts for the past 15 years. For example, our aggressive growth portfolio has helped ourselves and many around us to consistently maximize return with minimal drawdowns.

Lastly, do not hesitate to take advantage of the free-trials - they are absolutely 100% Risk-Free.

This article was written by

Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

source: https://seekingalpha.com/article/4491892-tesla-stock-buy-3-reasons-to-break-wrights-law

Your content is great. However, if any of the content contained herein violates any rights of yours, including those of copyright, please contact us immediately by e-mail at media[@]kissrpr.com.